On Friday, Altria finally completed its long awaited spin-off which gave each shareholder one share of Philip Morris International for every share of Altria owned. With the break-up there are now two potential buying opportunities in my opinion. Cramer depicts a choice between value (Altria) and growth (PMI), and I think he is dead on with this assessment, however I do believe one will perform better over time. Altria may not have the growth potential, but because the expectations are not as high I believe it will deliver results. Don't forget about the 5.2% dividend too which will attract a lot of value institutional investors. There are potential risks though, like dramitic decreases in sales in the United States, higher tax rates, and litigation. For many previous shareholders like myself the spin-off offers some much needed diversification so choosing one is not in the cards. Like Cramer says in his Mad Money clip (click title) both investments are solid long-term plays that will benefit from shareholder friendly management.

*Disclaimer: I own MO and PMI

Saturday, March 29, 2008

Friday, March 28, 2008

And the winner is...

Congrats to the winning team and to all of the finalists at the 2nd Annual MII Stock Pitch Competition.

Thursday, March 27, 2008

THL and Bain Sue Banks To Overpay

The LBO of Clear Channel Communications has been the bumpiest deal in while, with THL and Bain filing suits to force the banks funding the deal to pay up. Below is the document filed in NY:

CCU NY Lawsuit

via Dan P of PEHub

CCU NY Lawsuit

via Dan P of PEHub

Guess What? No Recession in Q4.

Today we got the final GDP numbers for Q4 2007, and to the relief of many, including the stock markets where futures rallied on the data, we did not enter a recession during Q4 (if one sticks with the typical definition of negative GDP growth). Instead, we saw a significantly slower growth number, 0.6%, than we had in Q3, 4.9%, but it should be considered that Q1 2007 also posted only 0.6% growth. We spent the next two quarters booming in real terms.

The obvious takeaway is that GDP growth fluctuates like the wind blows, and a slowdown is nothing to be afraid of or cry over. In fact, a list of the last 12 quarters of GDP growth shows exactly these back-and-forth swings I'm talking about; starting with Q1 2005 and going to Q4 2007: 3.7, 2.8, 4.4, 1.1, 4.8, 2.4, 1, 2, 0.6, 3.8, 4.9, 0.6. Now obviously the Q4 number can't speak for the Q1 2008 number (which we'll get our first look at on April 30), but a 0.6% rather than something with a "-" in front does put to rest all the talk that we entered a recession late in 2007 with the awful jobs data from December. This was the view espoused by Nouriel Roubini, Jim Cramer, and a few others who have correctly predicted 10-out-of-the-last-2 recessions.

Jobless claims were also solid today and PCE (personal consumption expenditures) were higher than some expected. Both contributed to the rally in stock futures.

The obvious takeaway is that GDP growth fluctuates like the wind blows, and a slowdown is nothing to be afraid of or cry over. In fact, a list of the last 12 quarters of GDP growth shows exactly these back-and-forth swings I'm talking about; starting with Q1 2005 and going to Q4 2007: 3.7, 2.8, 4.4, 1.1, 4.8, 2.4, 1, 2, 0.6, 3.8, 4.9, 0.6. Now obviously the Q4 number can't speak for the Q1 2008 number (which we'll get our first look at on April 30), but a 0.6% rather than something with a "-" in front does put to rest all the talk that we entered a recession late in 2007 with the awful jobs data from December. This was the view espoused by Nouriel Roubini, Jim Cramer, and a few others who have correctly predicted 10-out-of-the-last-2 recessions.

Jobless claims were also solid today and PCE (personal consumption expenditures) were higher than some expected. Both contributed to the rally in stock futures.

Wednesday, March 26, 2008

Santelli & Wesbury on CNBC

(Click Here for Video)

Rick Santelli discusses the "not pretty" durable goods report today. Brian Wesbury explains his rationale for still not falling into the recessionista's camp, and the CEO of AFLAC agrees with him.

Tuesday, March 25, 2008

Some See War. Others See Opportunity.

Iraq-Focused Hedge Fund Rebounds In February

March 25, 2008

After getting off to a slow start in January, Godvig Capital’s US$15.4 million Iraq-focused Babylon Fund rebounded nicely last month to the tune of 10.3%.

All asset classes in the portfolio, including Iraqi bonds, oil equities and banking stocks, contributed to the fund’s rebound, according to portfolio manager Björn Englund.

“During the month we maintained our prime investment strategy to increase our fund's exposure in a broad-based manner into what we regard as undervalued blue chips on the Iraqi Stock Exchange,” Englund wrote in an investor letter. “Beyond what most market participants (still too often inexperienced and trend-following though) regard as obvious opportunities, we also start to scan for new opportunities in the pre-IPO market.”

Englund remains optimistic on the “normalization” of Iraq’s economic future noting the formation of a “functioning shadow market, with characteristics of OTC-structure” and a planned secondary market trading of bonds and T-bills. “Perhaps the best (?) sign of normalization took place recently; the first underground hard metal concert in Baghdad,” he notes.

via FINAlt

March 25, 2008

After getting off to a slow start in January, Godvig Capital’s US$15.4 million Iraq-focused Babylon Fund rebounded nicely last month to the tune of 10.3%.

All asset classes in the portfolio, including Iraqi bonds, oil equities and banking stocks, contributed to the fund’s rebound, according to portfolio manager Björn Englund.

“During the month we maintained our prime investment strategy to increase our fund's exposure in a broad-based manner into what we regard as undervalued blue chips on the Iraqi Stock Exchange,” Englund wrote in an investor letter. “Beyond what most market participants (still too often inexperienced and trend-following though) regard as obvious opportunities, we also start to scan for new opportunities in the pre-IPO market.”

Englund remains optimistic on the “normalization” of Iraq’s economic future noting the formation of a “functioning shadow market, with characteristics of OTC-structure” and a planned secondary market trading of bonds and T-bills. “Perhaps the best (?) sign of normalization took place recently; the first underground hard metal concert in Baghdad,” he notes.

via FINAlt

Is This A School Or A Bank?

"It looks like MIT is moonlighting as an private fund fund-of-funds manager. The university’s investment office revealed in a recent regulatory filing that it has secured around $190 million in commitments for something called MIT Private Equity Fund IV, which apparently is the continuation of a program that quietly launched eight years ago.

I emailed someone in MIT’s investment office about the effort, and got this reply: 'Yes, we have a small FoF operation investing others’ capital alongside MIT’s, only in the private equity space. Investors are smaller endowments and foundations – basically 501c3s.'"

Placement Docs for MIT Private Equity Fund IV

Via Dan Primack of PEHub

I emailed someone in MIT’s investment office about the effort, and got this reply: 'Yes, we have a small FoF operation investing others’ capital alongside MIT’s, only in the private equity space. Investors are smaller endowments and foundations – basically 501c3s.'"

Placement Docs for MIT Private Equity Fund IV

Via Dan Primack of PEHub

Mortgage rates lag the Fed funds rate

A couple days ago there was a post on the blog about mortgage rates being the key to economic recovery, and if this is so then there is evidence that the Fed funds rate reductions are working. Mortgage rates are decreasing as are most rates across the board, however the mortgage rates are not adjusting as quickly as one would hope to the rate reductions at the Fed. If indeed, economic recovery lies with mortgage rates we will have to wait until they catch up.

Monday, March 24, 2008

Does flow of funds mark the bottom?

According to AMG Data Services, via FT Advisors, last week marked the first week in months where there was a net inflow of funds into equities. In fact, the turn around was quite large... a net inflow of $22.9B vs. a net outflow the week before of $1.4B. Likewise, bonds saw a net outflow of $423M last week vs. a net inflow of $1.3B the week before.

Rick Santelli Needs a reality show!

Rick Santelli joined CNBC Business News as on-air editor in June 1999, reporting live from the floor of the Chicago Board of Trade. His focus is primarily on interest rates, foreign exchange, and the Federal Reserve.

A veteran trader and financial executive, Santelli has provided live reports on the markets in print and on local and national radio and television. He joined CNBC from the Institutional Financial Futures and Options at Sanwa Futures, L.L.C. There, he was a vice president handling institutional trading and hedge accounts for a variety of futures related products.

Prior to that, Santelli worked as vice president of Institutional Futures and Options at Rand Financial Services, Inc., served as managing director at the Derivative Products Group of Geldermann, Inc., and was Vice President in charge of Interest Rate Futures and Options at the Chicago Board of Trade for Drexel, Burnham, Lambert. Santelli began his career in 1979 as a trader and order filler at the Chicago Mercantile Exchange in a variety of markets including gold, lumber, CD's, T-bills, foreign currencies and livestock.

He is a graduate of the University of Illinois Champaign/Urbana with a Bachelor of Science degree. Santelli has been a member of both the Chicago Mercantile Exchange and the Chicago Board of Trade.

Take a look at the following videos.

Video

Video

Video

Sunday, March 23, 2008

The Key to Recovery is...

Bill Gross, of PIMCO, the authority on bonds, says that the path to recovery is where this financial crisis started; the housing market. While most analysts forecast a continuing decline in housing prices for the rest of 2008, the severity of this decline will impact the spending power of many individuals. Many individuals hold the majority of their wealth in homes and in the last couple of years we have seen a significant decrease in that wealth, however the decline in housing prices and the Fed's willingness to cut rates has lowered mortgage rates. This will make buying homes more attractive therefore decreasing homes for sale on the market. At the same time, these new homeowners are getting in at lower prices which creates the opportunity for high wealth creation in their homes. The 30 year mortgage rate is the home financing unit of choice and the lower this rate goes the quicker we will get back to a more stable economy.

Bill Gross offers more opinions on the dollar, muni's, Fed actions, etc. Click the title for his investment outlook.

Desperate Times

From a CNBC article:

Kim Foss Erickson, a financial planner in Roseville, Calif., north of Sacramento, said she has never seen older children, even those in their 50s, depending so much on their parents as in the last six months.

Kim Foss Erickson, a financial planner in Roseville, Calif., north of Sacramento, said she has never seen older children, even those in their 50s, depending so much on their parents as in the last six months.

You know times are bad when you see dislocation like this. I think this story is humourous, but at the same time you have to give her credit for having the courage to make a tough decision that has major negative social ramifications.

Saturday, March 22, 2008

How Much To Invest?

One of the most difficult questions in investing is when you find a stock you like, how much do you put in?

Most people determine this based on their conviction; The more confident I am about a stock's performance, the greater the weight it will have in my portfolio.

I offer you a more methodical strategy. Enter the "Kelly Rule".

"How much should I stake - Kelly's strategy

The answer to this question has quite surprisingly been around for ages though it is discussed, analysed and refined often. Named after its author, John L Kelly Jr, if was first published in 1956.

Quite simply, the strategy enables you to find the answer to a question that is common amongst speculators and gamblers. If you have a bank of X, how much should you stake on each occasion to maximise your gain but minimise your loss so that in the long run you can perpetually increase your wealth!

Kelly considered the strategy of betting a fixed fraction of the bank on each occasion. In a favourable game, your fortune ought to grow exponentially, like compound interest. He worked out the way the rate of growth varied according to the fraction you bet. If you bet only a tiny fraction you will not go bankrupt but your wealth grows very little. Make the fraction large and the losses when they occur will wipe you out.

Kelly's answer was simple. The right balance is struck when the fraction you the fraction you bet exactly measures the size of your advantage. If you are being offered even money but the chance of an event occurring is 51% (and therefore the chance of failure is 49%) you should bet the difference between the two, 2%.

Therefore if you started with a bank of £100 and you correctly assessed your chances as discussed above you would need to place a bet of £2. Any higher and your probability of liquidation (risk) increases exponentially to your likely return."

Via Probability Theory

Most people determine this based on their conviction; The more confident I am about a stock's performance, the greater the weight it will have in my portfolio.

I offer you a more methodical strategy. Enter the "Kelly Rule".

"How much should I stake - Kelly's strategy

The answer to this question has quite surprisingly been around for ages though it is discussed, analysed and refined often. Named after its author, John L Kelly Jr, if was first published in 1956.

Quite simply, the strategy enables you to find the answer to a question that is common amongst speculators and gamblers. If you have a bank of X, how much should you stake on each occasion to maximise your gain but minimise your loss so that in the long run you can perpetually increase your wealth!

Kelly considered the strategy of betting a fixed fraction of the bank on each occasion. In a favourable game, your fortune ought to grow exponentially, like compound interest. He worked out the way the rate of growth varied according to the fraction you bet. If you bet only a tiny fraction you will not go bankrupt but your wealth grows very little. Make the fraction large and the losses when they occur will wipe you out.

Kelly's answer was simple. The right balance is struck when the fraction you the fraction you bet exactly measures the size of your advantage. If you are being offered even money but the chance of an event occurring is 51% (and therefore the chance of failure is 49%) you should bet the difference between the two, 2%.

Therefore if you started with a bank of £100 and you correctly assessed your chances as discussed above you would need to place a bet of £2. Any higher and your probability of liquidation (risk) increases exponentially to your likely return."

Via Probability Theory

Peak Oil Theory

There has been a lot of discussion on the blog concerning oil prices and the next direction they will take. Peak oil theory posits that a scare supply leads to a permanently higher price level and there are many supporters of this theory. However there is plenty empirical evidence to combat this theory like technological advances mentioned in the post above, but that does not mean the theory should be discredited. Personally the theory seems rational and fits basic supply/demand models, but the theory is very simple in that it doesn't take into account exogenous variables that could potentially create problems with the model. I think an important thing to remember is that many of the predictions and opinions we hear on oil are based on a multitude of models none of which are completely comprehensive.

Friday, March 21, 2008

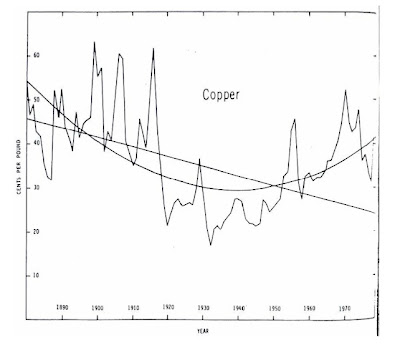

Quadratic Commodities

In response to Kyle Wolfe's post about the "commodity bubble":

Prices in scarce commodity markets follow two distinct trends (Margaret Slade):

Hotelling effect:

long-term scarcity results in prices

that increase over time.

Innovation effect:

technological innovations reduce

exploration and extraction costs;

results in prices that decrease over time.

What does the evidence suggest?

Answer: Both trends are apparent in the data.

As a result, they follow the following price paths:

For Copper:

For Silver:

Petroleum, follows a similar path. As seen in the graph in Wolfe's post below, we are clearly on the later part of the trend.

Thanks to Michael Moore.

Prices in scarce commodity markets follow two distinct trends (Margaret Slade):

Hotelling effect:

long-term scarcity results in prices

that increase over time.

Innovation effect:

technological innovations reduce

exploration and extraction costs;

results in prices that decrease over time.

What does the evidence suggest?

Answer: Both trends are apparent in the data.

As a result, they follow the following price paths:

For Copper:

For Silver:

Petroleum, follows a similar path. As seen in the graph in Wolfe's post below, we are clearly on the later part of the trend.

Thanks to Michael Moore.

A New Era Of Lending

"Activist hedge fund Pershing Square Capital Management has extended a $42.5 million lifeline to Borders Group, as the country’s second-largest bookseller put itself up for sale.

The New York-based hedge fund lent the money to Borders, in which it holds an 18% stake, after the Ann Arbor, Mich.-based company was unable to obtain necessary financing from its banks, Bank of America and JPMorgan Chase."

Focus on the second paragraph...

via FinAlt

The New York-based hedge fund lent the money to Borders, in which it holds an 18% stake, after the Ann Arbor, Mich.-based company was unable to obtain necessary financing from its banks, Bank of America and JPMorgan Chase."

Focus on the second paragraph...

via FinAlt

Thursday, March 20, 2008

Commodity Bubble?

Amid economic turmoil we have seen a substantial rise in commodity prices as many investors see them as a hedge against a slowing economy. What is going to happen when GDP growth rebounds to its average levels? Will investors flee and prices collapse? I don't know but click the title for an interesting article from the Economist about the growing Chinese appetite for commodities.

An excerpt:

...China is still just one of many countries looking for raw materials around the world. It has won most influence in countries where Western governments were conspicuous by their absence, and where few important strategic interests are at stake.

An In-Depth Look at Oil and Interest Rates

For those interested in Weijia's posts regarding Oil prices, please see below.

Oil prices tend to follow the Hotelling Model, described as:

pt – c = (p0 – c)(1+r)^t t=1,…,T-1, T

Notation:

qt = quantity depleted (used, consumed)

in time t

B(qt) = benefit function

c = marginal extraction cost

cqt = total extraction cost at time t

pt = resource price in time t

r = interest rate

S0 = stock available at time 0

T = exhaustion date

Where two conditions hold:

(1) price rises to the “choke price”

pT = pc [QD(pc) = 0]

(2) entire stock is just exhausted

∑T-1 qt + qT = S0

Additionally, Michael Moore brings up the "Arbitrage notion": rate of return in all physical asset markets equals rate of return on all financial instruments. Think about it...

Oil prices tend to follow the Hotelling Model, described as:

pt – c = (p0 – c)(1+r)^t t=1,…,T-1, T

Notation:

qt = quantity depleted (used, consumed)

in time t

B(qt) = benefit function

c = marginal extraction cost

cqt = total extraction cost at time t

pt = resource price in time t

r = interest rate

S0 = stock available at time 0

T = exhaustion date

Where two conditions hold:

(1) price rises to the “choke price”

pT = pc [QD(pc) = 0]

(2) entire stock is just exhausted

∑T-1 qt + qT = S0

Additionally, Michael Moore brings up the "Arbitrage notion": rate of return in all physical asset markets equals rate of return on all financial instruments. Think about it...

Interest Rates and Oil

This is just a brief follow up on my post on last Wednesday about oil. Similar to the interest rate theory discussed in David's post about OPEC & the Fed below, here are some interesting articles about the recent falling price of oil in relations to our economy, and how the Fed's less than expected interest rate cut has affected commodity prices.

OPEC & the Fed

A Solution of Sorts

Here is an intriguing pair of articles I ran across this morning. Jeff Frankel argues that the high prices of commodities like oil are being driven by low real interest rates. Anil Kashyap and Hyun Song Shin say that with oil prices so high, Middle Eastern sovereign wealth funds should come to the rescue of Wall Street.Put together, they suggest a new piece of the monetary transmission mechanism: The Fed's monetary expansion reduces interest rates, low interest rates drive up commodity prices, high commodity prices make OPEC rich, and finally OPEC uses its new wealth to recapitalize our struggling financial institutions.

Wednesday, March 19, 2008

U.S. Liquidity Trap

As pointed out by Paul Krugman on his blog, we may be quite close to a liquidity trap (read: Japan in 90s). The closing rates today for the 1 month and 3 month t-bills are 0.26 and 0.61 respectively. This leaves the Fed with little room to cut short term rates and at this point traditional monetary policy (open-market operations) essentially stops working. With a "slowing" economy and the financial markets having liquidity problems of their own (which is largely the reason t-bills have such low yields), this is quite a worrying sign.

Best Buyout

Even as the economy slows (consumer spending following!), Best Buy has found another reason to not bring in operations consultants, to not buy back stock, and to not clean up their balance sheet. What do they do? Start a VENTURE CAPITAL FIRM! Yes, that's right...the ailing electronics retailer is now in the VC game.

Best Buyout

via CEPro

Best Buyout

via CEPro

Tuesday, March 18, 2008

FDIC for I-Banks

The events leading up to Bear Stearns’ deal with JPMorgan were essentially a run on a non-commercial bank. As rumors spread that Bear Stearns would not be able to meet its obligations in part due to its exposure to the being-liquidated-as-we-speak Carlyle Capital, everyone starting pulling out their money and decreasing any exposure they may have had to the firm. In the first half of the 20th century, the federal government dealt with runs on commercial banks by creating the FDIC through the Glass-Steagall Act. Why not insure investment banks and certain other financial institutions in a similar manner?

There are obvious problems with insuring investment banks, such as the fact that this would require increased regulation of their balance sheets, not to mention capital reserve requirements on some assets that cannot realistically be valued.

Despite this, the Federal Reserve did essentially just that with Bear Stearns. Since the Fed could not afford to have the firm default on its obligations due to the potential impact on the already bloodied credit markets, it chose an acquisition of the company by JPMorgan. The Fed could not directly insure the most toxic elements of Bear’s book because it is not a commercial bank, but has basically done that to the tune of $30 billion for those same assets now that they’re on JPMs balance sheet.

Furthermore, the ~$2.33/share deal (based on JPM closing price of $42.71) for the 85-year-old investment bank seems a steal by most metrics, thus it appears reasonable that another buyer may emerge. While everyone waits for a new suitor, JPMorgan acts as the buyer of last resort. It cannot back down from the deal due to the fact that there is no material adverse change clause written in. This is similar to how insurance works. If all goes well (someone else acquires Bear or through some miracle it stands on its own two feet) everyone parts their ways and all liabilities are paid off. But if more shit hits the fan and no one wants to touch it, JPM buys it for nothing and similarly follows through on Bears obligations.

I am generally not keen on regulation but history is littered with liquidity crises of financial institutions. Why has no one come up with a way for the federal government to systematically insure regulated financial institutions other than commercial banks? Insuring I-banks is fraught with problems, but why not insure portions of their balance sheets, such as against counter-party risk on certain derivatives to help prevent liquidity crises?

There are obvious problems with insuring investment banks, such as the fact that this would require increased regulation of their balance sheets, not to mention capital reserve requirements on some assets that cannot realistically be valued.

Despite this, the Federal Reserve did essentially just that with Bear Stearns. Since the Fed could not afford to have the firm default on its obligations due to the potential impact on the already bloodied credit markets, it chose an acquisition of the company by JPMorgan. The Fed could not directly insure the most toxic elements of Bear’s book because it is not a commercial bank, but has basically done that to the tune of $30 billion for those same assets now that they’re on JPMs balance sheet.

Furthermore, the ~$2.33/share deal (based on JPM closing price of $42.71) for the 85-year-old investment bank seems a steal by most metrics, thus it appears reasonable that another buyer may emerge. While everyone waits for a new suitor, JPMorgan acts as the buyer of last resort. It cannot back down from the deal due to the fact that there is no material adverse change clause written in. This is similar to how insurance works. If all goes well (someone else acquires Bear or through some miracle it stands on its own two feet) everyone parts their ways and all liabilities are paid off. But if more shit hits the fan and no one wants to touch it, JPM buys it for nothing and similarly follows through on Bears obligations.

I am generally not keen on regulation but history is littered with liquidity crises of financial institutions. Why has no one come up with a way for the federal government to systematically insure regulated financial institutions other than commercial banks? Insuring I-banks is fraught with problems, but why not insure portions of their balance sheets, such as against counter-party risk on certain derivatives to help prevent liquidity crises?

Legalized Monopolies.

"The CME-Nymex deal would create a company that controls about 98 per cent of US-listed futures and offers contracts on a wide range of underlying commodities and events such as interest rates, foreign exchange, stock indices, oil, metals and agricultural products."

via FT

via FT

Monday, March 17, 2008

Market Predictions for Fed Cut

From the Cleveland Fed: The market is pricing in about a 35% chance for a 75bps cut tomorrow, followed by about a 25% chance for a 100bps cut. There is about a 20% implied probability for a 50bps cut, meaning that there is near certainty the Fed will bring rates down to at least 2.5%.

Economists with Attitude (EWA)

Click here for a great video that is making its way around the internet featuring Economists with Attitude, and among other things, their first smash hit, "Straight outta Lorch Hall."

Click here for a great video that is making its way around the internet featuring Economists with Attitude, and among other things, their first smash hit, "Straight outta Lorch Hall."

Sunday, March 16, 2008

Bear Buyout?

JP Morgan is negotiating a deal to buyout troubled investment bank Bear Stearns for around $20/share. This is 1/3 less than the current trading price of $30 which is indicative of how bad things are for Bear. The deal is in hurry-up mode because they want to get something done before the Asian markets open tonight. Even if they do get it done I still think we see some blood in Asia because the damage in the credit crisis has spread into a new domain. Not many saw this modern version of a bank run coming, and this could be a clear indicator of a recession. The proposed deal is worth $2.2 B (Bear's real estate is worth $1.2B). You know things are bad when the real estate you own is worth more than your business!

UPDATE: http://www.cnbc.com/id/23663919

The deal was announced for $2/ share or roughly $236 MM. In addition for every share of Bear Stearns owned investors will receive 0.05473 shares of JP Morgan. This price is the epitome of a "fire sale" price and is downright scary if you ask me. Many people want to know the true value of many financial service companies' balance sheets. Well here you go and I don't think this is a unique situation. Meanwhile markets are down in Asia which will probably be the same case here in the morning. Word of advice: Sleep in tomorrow and when you do wake up don't check your portfolio unless that is you want to buy more.

UPDATE: http://www.cnbc.com/id/23663919

The deal was announced for $2/ share or roughly $236 MM. In addition for every share of Bear Stearns owned investors will receive 0.05473 shares of JP Morgan. This price is the epitome of a "fire sale" price and is downright scary if you ask me. Many people want to know the true value of many financial service companies' balance sheets. Well here you go and I don't think this is a unique situation. Meanwhile markets are down in Asia which will probably be the same case here in the morning. Word of advice: Sleep in tomorrow and when you do wake up don't check your portfolio unless that is you want to buy more.

1,000 Lb Gorilla Seen In "Four Seasons"

"But competition could come much sooner from some of the CME’s own customers as a dozen brokerage firms are pushing a plan to launch an exchange, dubbed ELX, to rival the CME in U.S. Treasury futures trading.

Initially known as “Four Seasons,” ELX is backed by Bank of America, Barclays Bank, Citadel Investment Group, Citigroup, Credit Suisse, Deutsche Bank, eSpeed, GETCO, JPMorgan Chase & Co., Merrill Lynch & Co., PEAK6 Investments, and The Royal Bank of Scotland Group.

ELX, which stands for Electronic Liquidity Exchange, will run on eSpeed’s trading system and is entering agreements with technology firms to ensure broad customer access to its platform.

An executive for a firm in the Four Seasons group, who asked not to be named, said in an interview at the FIA that ELX is looking for more partners, in particular on the investment banking side, which may include large Treasury futures participants such as Goldman Sachs & Co. and UBS.

Some of the ELX firms, including Citadel, Credit Suisse and JPMorgan, as well as Lehman Brothers Holdings, Newedge and UBS, are involved in a similar futures exchange project in Europe, codenamed “Rainbow,” which is still in early stage development."

via P&I

Initially known as “Four Seasons,” ELX is backed by Bank of America, Barclays Bank, Citadel Investment Group, Citigroup, Credit Suisse, Deutsche Bank, eSpeed, GETCO, JPMorgan Chase & Co., Merrill Lynch & Co., PEAK6 Investments, and The Royal Bank of Scotland Group.

ELX, which stands for Electronic Liquidity Exchange, will run on eSpeed’s trading system and is entering agreements with technology firms to ensure broad customer access to its platform.

An executive for a firm in the Four Seasons group, who asked not to be named, said in an interview at the FIA that ELX is looking for more partners, in particular on the investment banking side, which may include large Treasury futures participants such as Goldman Sachs & Co. and UBS.

Some of the ELX firms, including Citadel, Credit Suisse and JPMorgan, as well as Lehman Brothers Holdings, Newedge and UBS, are involved in a similar futures exchange project in Europe, codenamed “Rainbow,” which is still in early stage development."

via P&I

The Politics of Oil

With oil prices crushing inflation adjusted highs, many people are wondering what the next move in oil will be. Oil is obviously intertwined with politics and we will see a different political regime in office next year so the agenda they create will have major implications on the price of oil. Click the title for an article from the Washington Post that discusses the U.S. oil interests and the War in Iraq.

Friday, March 14, 2008

Feldstein scares the hell out of me...

... sort of. Some may recall that I cited NBER outgoing President Martin Feldstein in my January report. In January, Feldstein said he was not ready to declare recession in the US and that he wasn't so sure we were heading for one. Now he has this to say, and given that he's changed his tone so much, the content is even scarier. Also, given that I lack modeling capabilities, I am forced to forecast using other forecasts done by firms which I believe base their models on the correct set of underlying variables and dynamics. These forecasts I rely on have not been amended, so neither has mine.

... sort of. Some may recall that I cited NBER outgoing President Martin Feldstein in my January report. In January, Feldstein said he was not ready to declare recession in the US and that he wasn't so sure we were heading for one. Now he has this to say, and given that he's changed his tone so much, the content is even scarier. Also, given that I lack modeling capabilities, I am forced to forecast using other forecasts done by firms which I believe base their models on the correct set of underlying variables and dynamics. These forecasts I rely on have not been amended, so neither has mine.

This Week In SPACs

This week, Alternative Asset Management Acquisition Corp announced that the SPAC had agreed to acquire Halcyon Asset Management LLC. Halcyon is the second prominent hedge fund to come public via a merger with a Special Purpose Acquisition Company, or SPAC (GLG Partners listed on the NYSE a few months ago via acquisition by Freedom Acquisition Holdings, another SPAC). This method of listing is an interesting alternative to the regulation intensive IPO. Aside from extensive SEC filings, it has been pointed out (Ms. Silva) that BX and FIG, which went public via high priced IPOs, have seen their shares plummet, while GLG, which went public via a SPAC, listed at a relatively low price, and has since seen its shares rise more than 15%. Below is a presentation you should definitely take a look at, as it gives you the most information a non-accredited investor can obtain regarding the Firm's offerings.

The Low Down On Halcyon Asset Management LLC

The Low Down On Halcyon Asset Management LLC

On The Rise

"8:01AM NYMEX reports Feb 2008 volume averaged record 1.846 mln contracts per day, electronic volume increases 30% and trading volume increases 99% (NMX) 97.00 : Co announces average daily volume for February 2008 of 1.846 mln contracts, a 20% increase from 1.542 mln contracts per day in February 2007. NYMEX electronic volume on the CME Globex electronic trading platform was 783,212 contracts per day and represented a 30% increase over 600,953 contracts per day in February 2007 electronic volume. NYMEX floor-traded energy futures and options averaged 240,842 contracts per day for February 2008. COMEX electronic volume on CME Globex averaged 179,934 contracts per day and represented a 99% increase over 90,500 contracts per day in February 2007 electronic volume. COMEX floor-traded average daily volume was 42,147 contracts for February 2008. Average daily volume on NYMEX ClearPort was 506,841 contracts for February 2008, compared to 385,711 for February 2007, representing a 31% increase."

via Briefing.com

99% increase in trading volume...not too shabby...

via Briefing.com

99% increase in trading volume...not too shabby...

ETF Update: Eh?

Some believe the recent bull run in agriculture will continue; Others believe that speculators have poured into the market, creating a bubble of historic proportion. Well, retail investors, it's time to put you money where your mouth is...

"In Canada, Toronto-based ETF purveyor BetaPro Management Inc. introduced two leveraged ETFs, the Horizons BetaPro DJ-AIG Agricultural Grains Bull Plus ETF (ticker: HAU) and the Horizons BetaPro DJ-AIG Agricultural Bear Plus ETF (ticker: HAD). Both new ETFs, which will be based on the DJ-AIG Grains Sub-Index, began trading on the Toronto Stock Exchange on Wednesday [March 12].

According to a release from BetaPro, the ETFs are designed to offer long or short exposure to the DJ-AIG sub-index, made up of soybeans, corn and wheat. The Bull Plus vehicle is designed to deliver twice the daily performance of the sub-index, whereas Bear Plus offers twice the inverse daily performance. Both ETFs are denominated in Canadian dollars, but offer exposure to returns expressed in U.S. dollars via currency hedging."

via Lipper

"In Canada, Toronto-based ETF purveyor BetaPro Management Inc. introduced two leveraged ETFs, the Horizons BetaPro DJ-AIG Agricultural Grains Bull Plus ETF (ticker: HAU) and the Horizons BetaPro DJ-AIG Agricultural Bear Plus ETF (ticker: HAD). Both new ETFs, which will be based on the DJ-AIG Grains Sub-Index, began trading on the Toronto Stock Exchange on Wednesday [March 12].

According to a release from BetaPro, the ETFs are designed to offer long or short exposure to the DJ-AIG sub-index, made up of soybeans, corn and wheat. The Bull Plus vehicle is designed to deliver twice the daily performance of the sub-index, whereas Bear Plus offers twice the inverse daily performance. Both ETFs are denominated in Canadian dollars, but offer exposure to returns expressed in U.S. dollars via currency hedging."

via Lipper

Wednesday, March 12, 2008

My Two Cents on Black Gold

Oil reached another intra-day high today of $110 a barrel.

The obvious and most talked about question surrounding oil is if the current price is reasonable. Well, let's examine this question from a few perspectives.

First, let's consider supply and demand. According to recent data from the Energy Department's Energy Information Administration (EIA), crude supplies jumped by 6.2 million barrels last week, more than three times the projected 1.6 million barrels. Additionally, gasoline supplies increased by 1.7 million barrels, far exceeding the expected 300,000 barrels increase. Finally, there is a healthy amount of current U.S. inventory at 224 million barrels, which is 22.3 million barrels above last year and 18.6 million barrels above the 5-year average. Oil consumption is expected to decline within the next few months due to further deterioration of the U.S. economy and warmer weather. From underlying supply and demand fundamentals, we can generally conclude a well supplied market.

Second, let's examine OPEC. Last week, the cartel decided to leave current production levels unchanged. However, OPEC, along with the EIA, project a continual decrease in demand, and the federal agency predicts an increase in non-OPEC production for the next few months. It is unlikely the cartel will increase production at the next meeting, but current expectations provide some cushion.

Third, we need to talk about speculation. The ever weakening dollar is contributing to the high price of oil as investors seek safety in commodities to hedge against inflation. The depreciating value of the dollar also reprices oil, sending it through the roof. However, most investors are buying up oil because it is the bandwagon hot ticket. According to an article on oil from the Associated Press today, "many traders are buying simply because others are buying." No one really wants to miss an opportunity to bag the elephant, so everyone keeps on buying, unrelated to fundamentals, and mass psychology continues to push up prices.

Finally, what do industry experts, pundits, and academics have to say about this? In an interview last week with Maria Bartiromo, ExxonMobil CEO Rex Tillerson said the current market does not suffer from shortages, and the high price of oil does not reflect market fundamentals. Various fund managers have expressed their caution of commodities, especially oil, and many predicts a commodity bubble burst. I have exchanged comments with Ross School of Business Prof. Scott Masten, who specializes in transaction cost economics. With regards to interest rates and the theory of exhaustible resources, Prof. Masten states, "it is hard to rationalize the high prices [of oil] we are now seeing on the basis of scarcity. For a while, it seems like there was an imbalance between world-wide demand and extraction and transportation capacity that was keeping prices higher than they should be. But with the economy slowing, and no major supply disruptions, prices should be falling rather than rising."

My prudent conclusion: Oil prices will fall, at least in the short-term, but not dramatically. I would be interested in knowing other theories or futures predictions on oil.

The obvious and most talked about question surrounding oil is if the current price is reasonable. Well, let's examine this question from a few perspectives.

First, let's consider supply and demand. According to recent data from the Energy Department's Energy Information Administration (EIA), crude supplies jumped by 6.2 million barrels last week, more than three times the projected 1.6 million barrels. Additionally, gasoline supplies increased by 1.7 million barrels, far exceeding the expected 300,000 barrels increase. Finally, there is a healthy amount of current U.S. inventory at 224 million barrels, which is 22.3 million barrels above last year and 18.6 million barrels above the 5-year average. Oil consumption is expected to decline within the next few months due to further deterioration of the U.S. economy and warmer weather. From underlying supply and demand fundamentals, we can generally conclude a well supplied market.

Second, let's examine OPEC. Last week, the cartel decided to leave current production levels unchanged. However, OPEC, along with the EIA, project a continual decrease in demand, and the federal agency predicts an increase in non-OPEC production for the next few months. It is unlikely the cartel will increase production at the next meeting, but current expectations provide some cushion.

Third, we need to talk about speculation. The ever weakening dollar is contributing to the high price of oil as investors seek safety in commodities to hedge against inflation. The depreciating value of the dollar also reprices oil, sending it through the roof. However, most investors are buying up oil because it is the bandwagon hot ticket. According to an article on oil from the Associated Press today, "many traders are buying simply because others are buying." No one really wants to miss an opportunity to bag the elephant, so everyone keeps on buying, unrelated to fundamentals, and mass psychology continues to push up prices.

Finally, what do industry experts, pundits, and academics have to say about this? In an interview last week with Maria Bartiromo, ExxonMobil CEO Rex Tillerson said the current market does not suffer from shortages, and the high price of oil does not reflect market fundamentals. Various fund managers have expressed their caution of commodities, especially oil, and many predicts a commodity bubble burst. I have exchanged comments with Ross School of Business Prof. Scott Masten, who specializes in transaction cost economics. With regards to interest rates and the theory of exhaustible resources, Prof. Masten states, "it is hard to rationalize the high prices [of oil] we are now seeing on the basis of scarcity. For a while, it seems like there was an imbalance between world-wide demand and extraction and transportation capacity that was keeping prices higher than they should be. But with the economy slowing, and no major supply disruptions, prices should be falling rather than rising."

My prudent conclusion: Oil prices will fall, at least in the short-term, but not dramatically. I would be interested in knowing other theories or futures predictions on oil.

Nobel Prize in Private Equity

Guess who has a PE firm now? That's right...see below.

Generation Investment Management,

via The International Herald Tribune

Generation Investment Management,

via The International Herald Tribune

Tuesday, March 11, 2008

You won't see this on CNBC, but...

... not all economists say its "Doom and Gloom." Case in point, the respected Anderson Forecast from UCLA. "We don't see that [recession] happening," said Edward Leamer, director and co-author of the forecast released Tuesday. "This is a tough call, but I will be very surprised if this thing actually precipitates into recession."

... not all economists say its "Doom and Gloom." Case in point, the respected Anderson Forecast from UCLA. "We don't see that [recession] happening," said Edward Leamer, director and co-author of the forecast released Tuesday. "This is a tough call, but I will be very surprised if this thing actually precipitates into recession."Future Portfolio Managers

At a one-of-a-kind public elementary school on the South Side of Chicago each incoming 1st grade class gets $20,000 so that the students can pick stock and manage their portfolio! After they graduate from high school they give back some of their returns to the community and the rest goes to the schools funds. This money came from Princeton grad and Barack Obama friend John Rogers, chairman and chief executive of Ariel Capital Management, the Chicago-based money management firm.

LINK TO STORY

LINK TO SCHOOL WEBSITE

It might be the case that these kinds can't see farther away than stocks like Jones Soda, Crocs, Apple, McDonald's but hey with decent timing these stocks have been all stars. This type of school is breading future MII members.

LINK TO STORY

LINK TO SCHOOL WEBSITE

It might be the case that these kinds can't see farther away than stocks like Jones Soda, Crocs, Apple, McDonald's but hey with decent timing these stocks have been all stars. This type of school is breading future MII members.

11 Reasons to Short Berkshire...

...from Douggy Kass of TheStreet.com and SeaBreeze Capital Partners, a short-only equity fund. Kass is as timely and writes as lucidly as anyone out there. I highly recommend checking in on his column for TheStreet.com regularly. He will give you an opinion which often (correctly) runs counter to the mainstream thought of the day. His "Primer on and the Secular Case for Short Selling" is also good reading.

...from Douggy Kass of TheStreet.com and SeaBreeze Capital Partners, a short-only equity fund. Kass is as timely and writes as lucidly as anyone out there. I highly recommend checking in on his column for TheStreet.com regularly. He will give you an opinion which often (correctly) runs counter to the mainstream thought of the day. His "Primer on and the Secular Case for Short Selling" is also good reading.Not everyone has given up on the economy...

... even though it may be 'en vogue' to compare today's experiences to the Great Depression or the Stagflation '70s. An excerpt from FT Advisors' report on last week's poor employment data:

So far, the current shift in payroll growth pales by comparison [to the shifts during previous recessions], suggesting that the economy is not suffering as much as many fear. The last recession officially ended in November 2001 and since then payrolls have grown by an average of about 100,000 per month. In the past two months payrolls have dropped by an average of 43,000. The total swing is 143,000 and this represents a 1.7 million annual change or 1.2% of the total number of payroll jobs currently in existence. This is a significantly smaller shift than those that occurred in the recessions of 1990-91 or 2001.

Why? Well, one reason is that we may not really be in recession. Swings of 100,000 per month in jobs are barely above the level of statistical significance. Another reason is that we have seen a major shift in demographic factors.

So far, the current shift in payroll growth pales by comparison [to the shifts during previous recessions], suggesting that the economy is not suffering as much as many fear. The last recession officially ended in November 2001 and since then payrolls have grown by an average of about 100,000 per month. In the past two months payrolls have dropped by an average of 43,000. The total swing is 143,000 and this represents a 1.7 million annual change or 1.2% of the total number of payroll jobs currently in existence. This is a significantly smaller shift than those that occurred in the recessions of 1990-91 or 2001.

Why? Well, one reason is that we may not really be in recession. Swings of 100,000 per month in jobs are barely above the level of statistical significance. Another reason is that we have seen a major shift in demographic factors.

How can the economy still grow if payrolls are shrinking? The answer is productivity growth: more output per hour worked. For an historical example, we need look no further back than 2002 and the first half of 2003. During that 18-month period, payrolls declined by an average of 50,000 jobs per month (worse than the average in the past two months) while real GDP expanded at a 2% annual rate (matching our forecast for Q1).

Monday, March 10, 2008

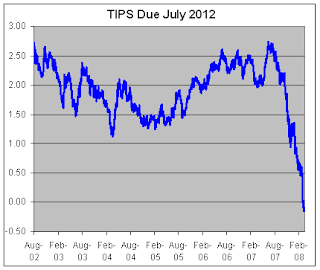

TIPS are now Negative

Treassury Inflation Protected Security (TIPS),securities whose principal is tied to the Consumer Price Index (CPI) due in June 2012 are now Yielding negative.

This means that investors are willing to take a negative real return in exchange for the (ahem) security of owning dollars.

Liquidity has dried up all over the world to such an extent that investors are willing to pay a huge "liquidity premium" (meaning, they can dump their TIPS whenever they want), that's greater than the real return of the bond.

Chart courtesy of crossingwallstreet.com

This means that investors are willing to take a negative real return in exchange for the (ahem) security of owning dollars.

Liquidity has dried up all over the world to such an extent that investors are willing to pay a huge "liquidity premium" (meaning, they can dump their TIPS whenever they want), that's greater than the real return of the bond.

Chart courtesy of crossingwallstreet.com

More Trouble Ahead? Ask The Options Guys...

The put/call ratio is on the rise again, something investors will want to keep an eye on!

Looking at the put/call ratio, we've see a recent rise into the 1.30 area - a critical level investors will want to keep an eye on. If the put/call ratio commences an extended move above 1.30, sellers could begin to hit the major indices hard.

Typically, the put/call ratio travels under 1, indicating bullish sentiment within the market, overall. However, given the present subprime debacle, elevated oil prices and waning economic conditions within America, Wall Street obviously has bearish cloud looming above head. Should the put/call ratio rally into the 1.5 area, expect fresh lows in the major indices.

via TraderDaily

Sunday, March 9, 2008

Jimmy Boy Runs His Mouth

Jim Cramer is becoming known for his little rants he pulls on TV nowadays and he did it again! This week's target: Hank Paulson, U.S. Secretary of Treasury. Cramer claims that Paulson can save a lot of potential problems by saying that the government will back up Fannie and Freddie paper, but it is very unclear if the government will buy some of these mortgages even though they are selling for relatively cheap. Buying the mortgages will settle some of the problems the markets are experiencing resulting less short term rate cuts will make the future battle on inflation much easier. Pretty soon Jim Cramer might not have any friends left on Wall Street.

Saturday, March 8, 2008

Mad Money?

“There is nothing that Cramer says that can help people make intelligent decisions. He takes something that is very serious and turns it into a game. If you want to have fun, go to Disney World.”

David F. Swenson, CIO of Yale endowment

David F. Swenson, CIO of Yale endowment

The Next Subprime

Subprime is apparently a two-part saga according to the performance of former Long-Term Capital Management partner John Meriwether.

"It isn’t quite déjà vu, but a hedge fund run by Long-Term Capital Management founder John Meriwether isn’t weathering the credit crisis well.

Meriwether’s Relative Value Fund is down 9.19% in the first two months of the year, his firm, Greenwich, Conn.-based JWM Partners, has told investors. The performance is the $1.2 billion fund’s worst since its 1999 launch.

In a note to investors in January, about one-third of the fund’s 4.14% decline that month was attributed to “an extreme spread widening in AAA commercial mortgage-backed securities,” Reuters reports."

via FinAlternatives.

"It isn’t quite déjà vu, but a hedge fund run by Long-Term Capital Management founder John Meriwether isn’t weathering the credit crisis well.

Meriwether’s Relative Value Fund is down 9.19% in the first two months of the year, his firm, Greenwich, Conn.-based JWM Partners, has told investors. The performance is the $1.2 billion fund’s worst since its 1999 launch.

In a note to investors in January, about one-third of the fund’s 4.14% decline that month was attributed to “an extreme spread widening in AAA commercial mortgage-backed securities,” Reuters reports."

via FinAlternatives.

Who's to Blame?

Obviously you can't place all the blame on the traders and bankers at many of the banks that announced large write downs, so what about the risk management department? Regulators from 5 countries put together a report that details the performance of the risk management divisions. It looks like they didn't perform up to standards.

More from BreakingViews:

http://www.breakingviews.com/2008/03/07/Credit%20spreads.aspx?email

http://www.breakingviews.com/2008/03/06/Buffett.aspx?email

http://www.breakingviews.com/2008/02/27/China%20oil.aspx?email

More from BreakingViews:

http://www.breakingviews.com/2008/03/07/Credit%20spreads.aspx?email

http://www.breakingviews.com/2008/03/06/Buffett.aspx?email

http://www.breakingviews.com/2008/02/27/China%20oil.aspx?email

Thursday, March 6, 2008

Thornburg Mortgage

Today was a horrible day for Thornburg Mortgage. Shares tanked 50% and they received many downgrades. Oh yeah and they are probably going to file for bankruptcy. Are we going to continue to see small mortgage houses like these go under in the future or is this just a one time deal. More stories like this can really have an impact of the direction of the market in the next couple of months.

Best of Buyouts

Via PEhub:

Last night was our 2nd Annual Buyouts Awards Dinner, as part of Buyouts East. What follows are your winners:

Buyout Firm Of The Year

The Blackstone Group

Deal of the Year

ACON Investments for GBarbosa

Mega Market Deal Of The Year

The Blackstone Group for Extended Stay Hotels

Large Market Deal Of The Year:

Lombard Investments for Dakota Minnesota and Eastern Railroad Corp.

Middle Market Deal Of The Year

Accel-KKR for Saber Holdings

Small Market Deal Of The Year

Halyard Capital for Tranzact

European Deal Of The Year

Advent International for Parques Reunidos

Emerging Market Deal Of The Year

ACON Investments for GBarbosa

Turnaround Of The Year

Sun Capital Partners for Mattress Firm

Large Lender Of The Year

Credit Suisse

Middle Market Lender Of The Year

GE Antares

Middle Market Investment Bank of The Year

Robert W. Baird & Co.

Law Firm Of The Year

Debevoise & Plimpton

Best New Firm

Alinda Capital Partners

Last night was our 2nd Annual Buyouts Awards Dinner, as part of Buyouts East. What follows are your winners:

Buyout Firm Of The Year

The Blackstone Group

Deal of the Year

ACON Investments for GBarbosa

Mega Market Deal Of The Year

The Blackstone Group for Extended Stay Hotels

Large Market Deal Of The Year:

Lombard Investments for Dakota Minnesota and Eastern Railroad Corp.

Middle Market Deal Of The Year

Accel-KKR for Saber Holdings

Small Market Deal Of The Year

Halyard Capital for Tranzact

European Deal Of The Year

Advent International for Parques Reunidos

Emerging Market Deal Of The Year

ACON Investments for GBarbosa

Turnaround Of The Year

Sun Capital Partners for Mattress Firm

Large Lender Of The Year

Credit Suisse

Middle Market Lender Of The Year

GE Antares

Middle Market Investment Bank of The Year

Robert W. Baird & Co.

Law Firm Of The Year

Debevoise & Plimpton

Best New Firm

Alinda Capital Partners

Wednesday, March 5, 2008

Wolverines in Private Equity

Which universities did private equity professionals at some of the largest firms attend?

Click Here to find out.

- Courtesy of Bankers Ball

Click Here to find out.

- Courtesy of Bankers Ball

Warren Buffett

Warren Buffett spent three hours on CNBC the other day and you can watch virtually all of it on cnbc.com. I would take advantage of that because he does a really good job explaining complicated things in layman's terms. One thing that really caught my attention was this quote:

"the stock market is there to serve you not to educate you."

What he means is that prices don't really tell you anything about a stock. The business of the company is what drives the price and when investing this is the most important aspect of any stock you should own. Obviously this is a very fundamentalist view, but can you argue with the results he has had?

"the stock market is there to serve you not to educate you."

What he means is that prices don't really tell you anything about a stock. The business of the company is what drives the price and when investing this is the most important aspect of any stock you should own. Obviously this is a very fundamentalist view, but can you argue with the results he has had?

How Flint, MI will spend the rebate $$$

I found it interesting that so many politicians and economists (including Bernanke) voiced support for a "rebate" to prop up the economy in classic demand-side fashion... until I remembered 2008 is an election year. The problem with the rebate program is that we've tried it before and we've found it to generate very little stimulus effect on the broader economy because people save it rather than spend it. The Flint Journal provides a great insight into this "phenomenon" with a recent article. An excerpt:

Nanny Marlena Robinette, 29, of Davison, already has a plan for the economic stimulus rebate check she'll receive this summer.

"I'm going to pay off bills," she said last week while shopping at Target in Flint Township.

Others, such as Judy France, 64, of Vienna Township plan to save it.

"I won't be spending the money," France said.

"I'm going to pay off bills," she said last week while shopping at Target in Flint Township.

Others, such as Judy France, 64, of Vienna Township plan to save it.

"I won't be spending the money," France said.

What is most insightful about this is where the article is coming from - FLINT and the GREATER-FLINT AREA - which is one of the most economically depressed areas in the country. If people aren't going to spend their rebate check there (the argument is that those most in need of help will be most likely to spend it), where will they?

Monday, March 3, 2008

UPDATE: MII Economic Forecast for 2008

In January we sent out a newsletter to the MII Hedge Fund Team with an economic forecast for Q4 2007 and FY 2008. What follows is a brief update on how that forecast has held up and some more specifics to add to it.

-------------------------------------

From the January forecast- Our call is for Q4 2007 to show growth around 0.5-1.5%, somewhat more moderate that the recent forecasts that we’ve already entered a recession...but significantly slower than the 4.9% growth seen in Q3. Q3 saw a big boom in export-led growth, and without a substantial rebound in the US$ over the last few months of the year one should expect similar results this time around.

Last week's preliminary data on Q4 GDP growth came in at 0.6% (unrevised from the 0.6% advance estimate released in January; GDP data for each quarter is released on an advanced, preliminary, and final basis coming a month apart from each another), which was towards the lower end of our estimate. This was a result of lower than expected growth in consumption which accounts for approximately 70% of all economic activity. As anticipated, growth in net exports (rising exports and falling imports) contributed significantly to GDP growth. What is surprising about this, however, is that the dollar was 'relatively' stable in Q4. The recent change in this factor carries positive implications for our Q1 forecast below.

-------------

From the January forecast- Our projection is for stagnant growth in Q1 and Q2 (0%-1%), followed by a rise in Q3 and Q4 to 1-2%. These projections are simply a blend of forecasts which fall in-line with our beliefs about the underlying fundamentals of the economy.

One of the forecasts which falls "in-line with our beliefs about the underlying fundamentals of the economy" comes from First Trust Advisors. FT Advisors recently released their updated forecast for Q1 2008, so its worth taking the time to note of any meaningful changes and to revise MII's forecast as necessary. GDP growth forecasts can be broken down into forecasts of consumption (70%), business investment (10%), government spending, net exports, housing (4%), and inventories. As FT Advisors notes in their report, government spending has accounted for approximately 0.3% growth over the last 5 years. Consistent fiscal policy suggests this will hold for Q1, so we start with 0.3% growth. MII breaks with FT Advisors in their forecast of consumption growth of 1.6% because the incoming data suggests more protracted weakness in consumer spending than anticipated by most economists. If we take a .8% increase in consumption rather than a 1.6%, and apply the 70% weight to this number, we arrive at .56%. So GDP growth now = (.3+.56) = 0.96. Housing looks to be the biggest drag on GDP growth once again, and FT Advisors forecasts a 24% drop in housing activity in Q1 for a weighted (4.1%) loss in GDP growth of 1%. MII will again forecast a greater decline in housing than FT, 30%, and will arrive at a weighted drag on GDP growth of 1.2%. So now GDP growth is 0.96-1.2= -0.24. Business investment has been sluggish in Q1 according to both surveys and purchasing data, so we forecast a paltry 1.5% growth weighted at 10.5%, resulting in a contribution to Q1 GDP growth of 0.1575. So our GDP growth estimate excluding only inventories and trade comes to a recession-like (-0.24 + 0.1575) = -0.0825. Inventories were down big in Q4, taking off 1.5% of GDP growth. Such a sustained drop in inventories cannot be expected to occur two quarters in a row even in the midst of a slowdown, so we side with FT in forecasting a modest build up contributing to 0.4% GDP growth (FT forecasts at 0.7% contribution). That puts us at a still-anemic (-0.0825 + 0.4) = 0.3125% GDP growth excluding trade. As anyone who has tuned into the financial news knows, the US$ has plummeted recently amid concerns about inflation and interest rate cuts. This should only make the trade numbers stronger in Q1, and here MII will agree with FT Advisors that export-led trade growth contributes 0.6% to GDP in Q1. Thus, including trade, MII forecasts GDP growth to be (0.3125 + 0.6) = 0.9125% in Q1 2008. This is nothing for consumers to cheer about, but it would probably be a pleasant surprise to be welcomed by financial markets which have discounted stocks to include an increased probability that Q1 saw negative or no GDP growth. Obviously then, our 0.9% estimate for Q1 GDP growth falls on the higher end of the January estimate (0-1%), and this can be attributed to the continued deterioration in the value of the US $ relative to its primary trading partners.

Risks to the downside include worse trade numbers due to higher oil prices in Q1 and even a sharper drop in consumption arising from the housing spillover. Also, the inflation numbers we've seen recently are more concerning than anticipated in MII's January forecast. While this may be a boost for trade and GDP in Q1 and Q2, one should be concerned about the viability of any economic strategy that relies inflating our way to prosperity.

Regardless of what the numbers turn out to be (we won't get the advance GDP estimate for Q1 until April 30), you can be sure that the stock and bond markets will react.

-------------------------------------

From the January forecast- Our call is for Q4 2007 to show growth around 0.5-1.5%, somewhat more moderate that the recent forecasts that we’ve already entered a recession...but significantly slower than the 4.9% growth seen in Q3. Q3 saw a big boom in export-led growth, and without a substantial rebound in the US$ over the last few months of the year one should expect similar results this time around.

Last week's preliminary data on Q4 GDP growth came in at 0.6% (unrevised from the 0.6% advance estimate released in January; GDP data for each quarter is released on an advanced, preliminary, and final basis coming a month apart from each another), which was towards the lower end of our estimate. This was a result of lower than expected growth in consumption which accounts for approximately 70% of all economic activity. As anticipated, growth in net exports (rising exports and falling imports) contributed significantly to GDP growth. What is surprising about this, however, is that the dollar was 'relatively' stable in Q4. The recent change in this factor carries positive implications for our Q1 forecast below.

-------------

From the January forecast- Our projection is for stagnant growth in Q1 and Q2 (0%-1%), followed by a rise in Q3 and Q4 to 1-2%. These projections are simply a blend of forecasts which fall in-line with our beliefs about the underlying fundamentals of the economy.

One of the forecasts which falls "in-line with our beliefs about the underlying fundamentals of the economy" comes from First Trust Advisors. FT Advisors recently released their updated forecast for Q1 2008, so its worth taking the time to note of any meaningful changes and to revise MII's forecast as necessary. GDP growth forecasts can be broken down into forecasts of consumption (70%), business investment (10%), government spending, net exports, housing (4%), and inventories. As FT Advisors notes in their report, government spending has accounted for approximately 0.3% growth over the last 5 years. Consistent fiscal policy suggests this will hold for Q1, so we start with 0.3% growth. MII breaks with FT Advisors in their forecast of consumption growth of 1.6% because the incoming data suggests more protracted weakness in consumer spending than anticipated by most economists. If we take a .8% increase in consumption rather than a 1.6%, and apply the 70% weight to this number, we arrive at .56%. So GDP growth now = (.3+.56) = 0.96. Housing looks to be the biggest drag on GDP growth once again, and FT Advisors forecasts a 24% drop in housing activity in Q1 for a weighted (4.1%) loss in GDP growth of 1%. MII will again forecast a greater decline in housing than FT, 30%, and will arrive at a weighted drag on GDP growth of 1.2%. So now GDP growth is 0.96-1.2= -0.24. Business investment has been sluggish in Q1 according to both surveys and purchasing data, so we forecast a paltry 1.5% growth weighted at 10.5%, resulting in a contribution to Q1 GDP growth of 0.1575. So our GDP growth estimate excluding only inventories and trade comes to a recession-like (-0.24 + 0.1575) = -0.0825. Inventories were down big in Q4, taking off 1.5% of GDP growth. Such a sustained drop in inventories cannot be expected to occur two quarters in a row even in the midst of a slowdown, so we side with FT in forecasting a modest build up contributing to 0.4% GDP growth (FT forecasts at 0.7% contribution). That puts us at a still-anemic (-0.0825 + 0.4) = 0.3125% GDP growth excluding trade. As anyone who has tuned into the financial news knows, the US$ has plummeted recently amid concerns about inflation and interest rate cuts. This should only make the trade numbers stronger in Q1, and here MII will agree with FT Advisors that export-led trade growth contributes 0.6% to GDP in Q1. Thus, including trade, MII forecasts GDP growth to be (0.3125 + 0.6) = 0.9125% in Q1 2008. This is nothing for consumers to cheer about, but it would probably be a pleasant surprise to be welcomed by financial markets which have discounted stocks to include an increased probability that Q1 saw negative or no GDP growth. Obviously then, our 0.9% estimate for Q1 GDP growth falls on the higher end of the January estimate (0-1%), and this can be attributed to the continued deterioration in the value of the US $ relative to its primary trading partners.

Risks to the downside include worse trade numbers due to higher oil prices in Q1 and even a sharper drop in consumption arising from the housing spillover. Also, the inflation numbers we've seen recently are more concerning than anticipated in MII's January forecast. While this may be a boost for trade and GDP in Q1 and Q2, one should be concerned about the viability of any economic strategy that relies inflating our way to prosperity.

Regardless of what the numbers turn out to be (we won't get the advance GDP estimate for Q1 until April 30), you can be sure that the stock and bond markets will react.

"How a Bubble Stayed Under the Radar"

by Yale economist Robert Shiller in yesterday's NYTimes. Shiller is a U of M alum, the co-founder of the Case-Shiller housing index, the author of "Irrational Exuberance," and a leading behavioral finance economist.

HT: Greg Mankiw

Crossing the Threshold

Are Americans finally cutting back on gasoline because of rising prices? The WSJ seems to think so. An excerpt:

Economists and policy makers have puzzled for years over what it would take to curb Americans' ravenous appetite for fossil fuels. Now they appear to be getting an answer: sustained pain.

People are starting to realize that these prices are here to stay for the long run which means that more cost efficient transportation will be used in the future. People will vacation less or vacation to places that aren't as far away. Also people will move closer to their jobs which could impact the way communities and cities are organized. These transitions are moving a little faster with the inflation numbers we are getting. Even core inflation advanced 2.5% from last year. What does this mean for commodity prices? This is a definite decrease in demand, but demand elsewhere is growing so the effect is ambiguous at best. Many experts predict $4/gallon gasoline in the summer, but I think drivers have had enough.

Economists and policy makers have puzzled for years over what it would take to curb Americans' ravenous appetite for fossil fuels. Now they appear to be getting an answer: sustained pain.

People are starting to realize that these prices are here to stay for the long run which means that more cost efficient transportation will be used in the future. People will vacation less or vacation to places that aren't as far away. Also people will move closer to their jobs which could impact the way communities and cities are organized. These transitions are moving a little faster with the inflation numbers we are getting. Even core inflation advanced 2.5% from last year. What does this mean for commodity prices? This is a definite decrease in demand, but demand elsewhere is growing so the effect is ambiguous at best. Many experts predict $4/gallon gasoline in the summer, but I think drivers have had enough.

No More Higher Taxes

Front page of the WSJ today talks about so called "McCainomics" put forth by Senator McCain. Taxes are always front and center in the race for the presidency. McCain wants to ensure that tax rates do not go up from their current positions, but in order to do that there must be substantial spending cuts from the government. Luckily McCain is a hawk on government spending shown through his policies while the senator of Arizona and will probably reduce the budget deficit if elected to the presidency. However, will this be enough? I don't think so because the gap is huge and his proposed actions on paper may add up, but will be a lot harder to push through Congress. For example he wants to get rid of the AMT, but doing so is very complicated because it creates a large deficit for the federal government. Even an attempt to modify the AMT will be costly for Washington because they have to get there money. Get ready for higher taxes.

Source: WSJ

*Might need subscription to read the article

Source: WSJ

*Might need subscription to read the article

Sunday, March 2, 2008

The Texas Two Step

This Tuesday the battle for the Democratic nomination heads to Ohio and Texas. Obama has been riding the momentum train and hopes to keep his winning streak alive. Wins in Ohio and Texas will be devastating to Hilary's campaign, but if she does lose she will mathematically still have a chance to get the delegates needed for the nomination. Last I heard, polls in Texas where fairly even but the popular vote doesn't guarantee the candidate all delegates. The Texas Two Step is a combination of a primary which has two-thirds of the delegates and a caucus which has one-third of the delegates. The primary is from 7am-7pm and the caucus is held just after the polls close. One candidate could win the popular vote and still not have the majority of the delegates because of how the delegates are determined. The dual delegate system gives the citizens of Texas the opportunity to vote twice which has been stressed by the supporters of both candidates. It should be interesting to see what happens on Tuesday.

Subscribe to:

Posts (Atom)

{kind=link}